|

| Graphic from Sprott Money. |

The rise in petroleum prices was a key element to the 2008 crisis, but would eventually bring something positive to the US. Petroleum is usually extracted from large underground cavities known as reservoirs. However, it is formed at greater depth, within source rocks, where organic matter is slowly cooked by the internal heat of the planet until it degrades, first into petroleum and finally into gas. Prices persistently above 100 dollars per barrel meant that beyond traditional reservoirs it also became feasible to drill deeper for petroleum, down to source rocks and other rock formations of low permeability.

In 2010 the US Government and media thus embarked in a promotional campaign for source rock drilling, erroneously calling "shales" to these resources to ease the marketing. Vast amounts of money started flowing to the sector, the industry quivered with activity, plenty of new jobs were created and the country soon emerged from economic recession. The end result: in three years petroleum extraction in the US grew by 50%, returning to levels not seen since the 1980s.

But there was a problem: extracting petroleum from source rocks requires a relentless effort, without parallel among the resources explored by the industry. While a well drilled into a traditional reservoir can extract petroleum for decades, a well drilled into source rocks looses half of the initial flow rate in just 12 months, having a mean lifetime of just three years. In consequence, a company operating on these resources must be permanently drilling new wells just to keep the volume of petroleum extracted constant. This kind of activity requires unusually high amounts of capital investment.

The American petroleum industry was able to source astronomical sums of money to keep the gargantuan "shale" machine running recurring to the debt bond market. With great help of the media, a swollen image of the real dimension of these resources was conveyed by the industry, in some cases announcing to investors reserves ten times larger than those reported to fiscal authorities. This practice yearned various suggestive names: "shale hype", or my preferred, "snake oil".

Bloomberg explained with this info-graphic how investors were lured into the "shale oil" hype.

Bloomberg explained with this info-graphic how investors were lured into the "shale oil" hype.

In the first half of 2014 the volume of debt issued by the global petroleum industry was equivalent to the GDP of Austria. In the US, the mismatch between the expanding bond market and realistic petroleum extraction perspectives has long been raising apprehension among energy analysts. For some it is visible that the volume of petroleum extracted from source rocks is to slow down and eventually stop growing around the 2015/2016 winter. It is hard to envision in this scenario how can the industry generate enough cash flows to sustain the amounts of debt it issued. In reference to this problem, I employed last Spring the term "shale sub-prime", drawing the parallel with the 2008 crisis.

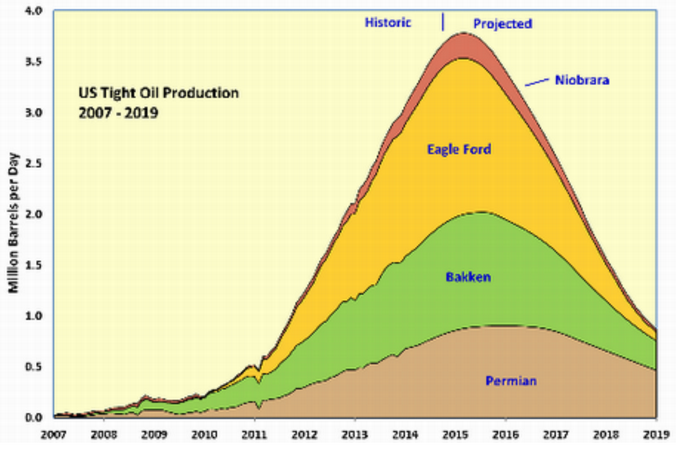

Petroleum extraction from source rocks as projected by David Archibald, one of many independent observers expecting these resources to peak in the short term.

Petroleum extraction from source rocks as projected by David Archibald, one of many independent observers expecting these resources to peak in the short term.

Throughout the past few months fear spread in the US stock market, with thousands of millions abandoning the energy sector. The alternative media percolates the information: a default tsunami is heading for shore. The question left to answer is how much of an impact will it have on the reminder of the economy, through the multiple banks and funds gripped by the "shale hype". Just as in 2008, the volume of financial products leveraged on the "shale sub-prime" is key to the answer.

In the so called "junk" bond market alone, rest presently 200 G$ (thousand million dollars) issued by petroleum companies. To this add debt instruments issued in other market segments, bonds issued by industries dependent on petroleum extraction (metallurgy, heavy machinery, sand extraction, logistics), plus leveraged products. In 2008, the "bail out" employed by the US government to save the financial sector from the housing "sub-prime" was 700 G$. The default deluge triggered by the "shale sub-prime" may not seem as large at this moment, but is certainly in the same order of magnitude.

As more information emerges, the moment of truth is slowly becoming visible. Petroleum companies must submit their 2014 asset reports to creditors until the end of March. Based on petroleum prices of late December, these assets are worth half of what they did one year before; moreover, it will make crystal clear to creditors that "shale oil" is a money losing business. The end of the first quarter is also a natural bond maturity epoch; it is thus not hard to perceive that by then many companies will simply not be able to roll over their debt. Bankruptcy is the likely end to many of them.

Quietly, observers write about a possible "shale bail out", even in the mainstream media. Independently of such being or not the final outcome, one thing is certain: just as in 2008, this crisis was perfectly visible from the distance.

But strangely enough, the market seems not to be aware of it yet :

ReplyDeletehttp://www.zerohedge.com/news/2015-02-03/energy-company-valuations-explode-dot-com-bubble-levels