The EIA published this week their petroleum extraction figures for September, presenting a world wide reduction of 0.5 Mb/d from August. This inversion into decline during the summer is now present in all publicly available datasets; the cries of "Peak Oil" grow louder. As usual I prefer a cautious tone, Iran, Iraq and Libya sum together several Mb/d of unrealised potential at this point; eventually it may invert the extraction profile once again. However, regarding where prices and stocks are presently, one can not possibly rule out 2015 as the terminal year for petroleum.

In spite of these data, in my view the Sunni-Shiite war in Iraq and Syria remained the major story of 2015. With dozens of countries involved in one way or another, this war is building into a focus of tension unprecedented since the Iranian revolution. The past few years I have tried in this reviewed to answer a simple question: is Europe on the right side in this war? But is it even clear on which side are we? The article that opens this last review of 2015 dives deep into this war, showing that things are not at all straightforward and that perhaps Europe is really wrong footed, embroiled into a trap of its own making.

An hiatus to the press review is likely to follow; details are at the end of this note.

26 December 2015

19 December 2015

Press review 19-12-2015 - Sour Christmas

Declining numbers of visits to this weblog tell me a lot folk are getting busy with Christmas, either travelling, shopping or both. However, this will be a bitter Christmas for many families that are one way or another dependent on the energy industry, petroleum and gas in particular. The US Federal Reserve flagged a major turning point this week with a return to interest rate hikes. Currencies and commodities sank against the dollar across the board, confirming that the current market is here to stay a while longer. Of the more than 300 000 folk that lost their jobs in this industry since 2014 few will ever make it back; search for a new a career they must.

Declining numbers of visits to this weblog tell me a lot folk are getting busy with Christmas, either travelling, shopping or both. However, this will be a bitter Christmas for many families that are one way or another dependent on the energy industry, petroleum and gas in particular. The US Federal Reserve flagged a major turning point this week with a return to interest rate hikes. Currencies and commodities sank against the dollar across the board, confirming that the current market is here to stay a while longer. Of the more than 300 000 folk that lost their jobs in this industry since 2014 few will ever make it back; search for a new a career they must.

I feel the best word to describe what is going on in middle management, administrative boards and petroleum ministries is panic. The market is out of control and no one - really no one - is safe at 37 $/b. From small to large companies, from multinationals to governments, everyone is bracing to what will be the deepest contraction of the petroleum (and gas) industry at least since 1985.

Here in Europe consumers are now paying the lowest prices in a decade for petrol and diesel. Enjoy it while you can. Petroleum will eventually come back in vengeance.

12 December 2015

Press review 12-12-2015 - Under 40 hangover

This week felt somewhat like an hangover from the hectic events of the previous week. The chaos in which the OPEC meeting of the 4th ended only produced its full effect this Monday, with another collapse in petroleum prices. The Brent index resisted for a few days, but would eventually break under 40 $/b, to close the week at 37 $/b. The media warns in unison of an impeding financial disaster with the energy industry; but so far banks keep feeding money to a large numbers of companies that are essentially dead. How will this all unfold is hard to tell at this moment, but some sort of bailout is more than likely - possibly through the banks themselves.

This week felt somewhat like an hangover from the hectic events of the previous week. The chaos in which the OPEC meeting of the 4th ended only produced its full effect this Monday, with another collapse in petroleum prices. The Brent index resisted for a few days, but would eventually break under 40 $/b, to close the week at 37 $/b. The media warns in unison of an impeding financial disaster with the energy industry; but so far banks keep feeding money to a large numbers of companies that are essentially dead. How will this all unfold is hard to tell at this moment, but some sort of bailout is more than likely - possibly through the banks themselves.

Meanwhile, the whole "peak is here" talk is back once again in the wake of a small decline in the global production of liquid agricultural products. In what fossil liquids - petroleums - are concerned, extraction is still growing strong; even though hard data for the last quarter is not yet there, preliminary assessments point to something very close to 81 Mb/d by now. From the summer of 2014 until now world petroleum extraction grew 5 Mb/d, more than it grew the whole decade before that.

However, I recognise 37 $/b will leave their mark. The petroleum industry is essentially shutting down, and even with Iraq and Iran replacing the coming extraction collapse in North America, the decline will eventually set in. It might become already visible in late 2016, but will be certainly marked in 2017 and 2018. Will that be the much dread "peak oil"? Far too early to tell.

05 December 2015

Press review 05-12-2015 - Eruption

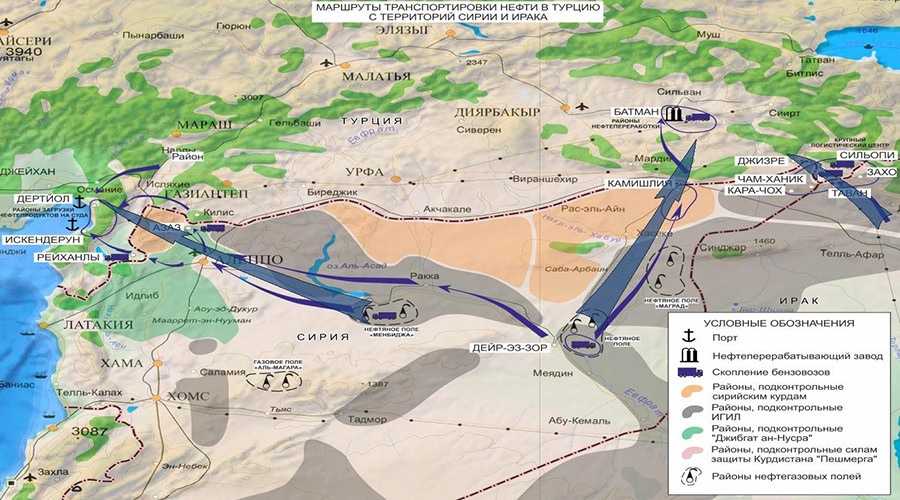

Once in a while an old meme pops up in the media claiming the war in Syria was caused by CO2. One may certainly wonder what sort of gases are making into the brains of some world leaders, but one thing is certain, regardless of how it started, the war in Syria and Iraq is being fuelled by petroleum. Far from surprising to regular readers, fresh claims from Iraq and Russia that Turkey is trading in crude from Daesh provide an important update: back in August the caliphate was selling over 200 kb/d.

The western media remains largely reluctant in reporting this aspect of Turkey's involvement in this war, and even goes as far as claiming that Daesh is actually selling petroleum to its Shiite foe in Syria... Even the claims on CO2 are more credible.

There has not been a week like this in quite a while, with relevant developments on almost every front. The world seems erupting and energy plays a central role, as always. Most remarkable this time is the rise in geo-political tension meeting a deeply depressed energy market.

The western media remains largely reluctant in reporting this aspect of Turkey's involvement in this war, and even goes as far as claiming that Daesh is actually selling petroleum to its Shiite foe in Syria... Even the claims on CO2 are more credible.

There has not been a week like this in quite a while, with relevant developments on almost every front. The world seems erupting and energy plays a central role, as always. Most remarkable this time is the rise in geo-political tension meeting a deeply depressed energy market.

28 November 2015

Press review 28-11-2015 - The other side of the barricade

I was born during the last years of the cold war, and even though I was quite young, I remember vividly the permanent tension between East and West, in particular through the conflicts in Africa and the Middle East. Even considering those times, I can not recall a military incident bringing these secular blocks so close to an armed conflict as that lived this week.

I was born during the last years of the cold war, and even though I was quite young, I remember vividly the permanent tension between East and West, in particular through the conflicts in Africa and the Middle East. Even considering those times, I can not recall a military incident bringing these secular blocks so close to an armed conflict as that lived this week.

In this sort of events there are usually two different sides of the same the story, not being easy to tell who is who. However, in this particular occasion it is rather easy, especially after the publication by the Turkish military of the map reproduced here. The invasive trajectory claimed in the Turkish account of events stretches for no more than two nautical miles. Even if this trajectory is correct, and even if the Su-24 was cruising at sub-sonic speeds, the Russian aircraft spent less than 15 seconds in Turkish air space. The Su-24 was shot down over Syrian territory and in all likelihood the Turkish F-16 entered there to do so.

Turkey is sending a message, not only to Russia, but in particular to its European NATO partners. Turkey is not willing to give hand of its acquired position in the region. It is not willing to give hand of the human, petroleum and arms trafficking businesses; it is not giving hand of its will to remove the Shiites from power in Syria; it is not willing to allow the rise of an autonomous Kurdistan; it is not giving hand of the will to expand further the territory it took from Syria after the II World War.

It is becoming clearer who is on the other side of the barricade. Rest to know if Europe remains committed to fight and win this war.

22 November 2015

Convergence Preview - 03 - Progress

Pretty amazing, I am actually writing this from a Chrubuntu install on the Tegra K1, and more spectacularly, with the Unity desktop environment. There is still a number of things malfunctioning, the road ahead is long, but this is a capital step in this project. Below the fold I detail this latest chapter of the story.

Pretty amazing, I am actually writing this from a Chrubuntu install on the Tegra K1, and more spectacularly, with the Unity desktop environment. There is still a number of things malfunctioning, the road ahead is long, but this is a capital step in this project. Below the fold I detail this latest chapter of the story.

But already one of the most important milestones in this project has been achieved: performance. As a matter of fact, I feel no difference in terms of interface usability in contrast to my usual work environment. Moving windows around, sending them to other workspaces, shifting between workspaces, using the HUD and Lenses, all is fast and fluid. The Tegra K1 is proving an able CPU for desktop work, but for a fraction of the cost, space and power.

21 November 2015

Press review 21-11-2015 - War

|

|

|

I live a few hundred meters from the French border, the state of emergency has been quite visible: heavily armed police in train stations, chronic traffic jams imposed by border checks. President Hollande was not exaggerating when he used the term war. But in face of the precipitous bombing of assorted targets in Raqqa, I wonder if the French government is exactly aware of the kind of war it is fighting.

I have postulated various times that geo-political events have more potential to shape the petroleum extraction curve in the short term than geology by itself.

14 November 2015

Press review 14-11-2015 - Peak Coal, says Greenpeace

Foreword: This review was written before the terror attacks yesterday night in Paris. This is incredibly sad; my thoughts are with the families that lost their loved ones. For long I have been reporting in this review that in these past few years Europe has been supporting the wrong side in various conflicts. There is no way to know if these attacks had taken place whether Libya and Syria were not at war. However, this is definitely the moment to rethink the foreign policy towards these neighbouring countries and jihadist organisations in general.

Coal was the big story this week. Within days of the graphs by Jean Laherrère on Coal extraction being published, the Greenpeace came out with a study confirming the terminal decline in the Middle Empire. But the environmentalist organisation goes further, claiming the rest of the world will not be able to make up for this decline. With this report the Greenpeace clearly distances itself from the IPCC and the IEA; this dose of realism is most refreshing.

However, the Coal news making the rounds is an article by the New York Times claiming the Chinese have under-reported their extraction and consumption figures by as much as 17%. Coincidentally, I am subscribed to an e-mail list where David Fridley explained how this American newspaper is simply comparing different figures reported by the Chinese institutions. But it is always interesting to know on which side the press is.

And the other big news of the week was a 10% decline in petroleum prices; the Brent index now stands at 44 $/b, the lowest level since 2009.

Coal was the big story this week. Within days of the graphs by Jean Laherrère on Coal extraction being published, the Greenpeace came out with a study confirming the terminal decline in the Middle Empire. But the environmentalist organisation goes further, claiming the rest of the world will not be able to make up for this decline. With this report the Greenpeace clearly distances itself from the IPCC and the IEA; this dose of realism is most refreshing.

However, the Coal news making the rounds is an article by the New York Times claiming the Chinese have under-reported their extraction and consumption figures by as much as 17%. Coincidentally, I am subscribed to an e-mail list where David Fridley explained how this American newspaper is simply comparing different figures reported by the Chinese institutions. But it is always interesting to know on which side the press is.

And the other big news of the week was a 10% decline in petroleum prices; the Brent index now stands at 44 $/b, the lowest level since 2009.

13 November 2015

David Fridley on Chinese Coal statistics

Almost simultaneously to the note with Jean Laherrère's graphs on Coal extraction, the New York Times published an article claiming China had been under-reporting their extraction and consumption figures. The opening words of this article were right to the point:

Days ago I received a message from David Fridley that brought this issue under a completely different light. David is a scientist at the China Energy Group, working and living in China the past 25 years. He was kind enough to consent the publication of his views in this space.

China, the world’s leading emitter of greenhouse gases from coal, has been burning up to 17 percent more coal a year than the government previously disclosed, according to newly released data.Although never questioning directly the 2013 peak, the article raised doubts on the declining trend setting in. More than anything else, the New York Times aims to hike the pressure on China in light of the coming world climate summit to be held in Paris (COP21).

Days ago I received a message from David Fridley that brought this issue under a completely different light. David is a scientist at the China Energy Group, working and living in China the past 25 years. He was kind enough to consent the publication of his views in this space.

07 November 2015

Press review 07-11-2015 - Autumn Blues

Days are getting shorter and shorter; at some point the clock goes back one hour and suddenly the faint autumn sun sets at five in the afternoon - in the rare days the sun is actually visible between the permanent clouds. For many folk (like me) this seasonal deprivation of natural light can induce depression, in varying degrees each year.

It is also by this time that another depressive story starts emerging: the growing difficulty to adequately supply Europe's energy grids. At the eye of the storm remains the UK, that faces increasing energy deprivation from left and right. The first scare of this season is already there, too soon and at too high temperatures for comfort.

It is also by this time that another depressive story starts emerging: the growing difficulty to adequately supply Europe's energy grids. At the eye of the storm remains the UK, that faces increasing energy deprivation from left and right. The first scare of this season is already there, too soon and at too high temperatures for comfort.

04 November 2015

Peak Coal In China and the World, by Jean Laherrère

I have been trying to follow the Coal story in China for more than two years, when a series of articles made me realise environmental impacts were creating serious obstacles to continued growth. Coal extraction in China peaked that same year, but is this new trend merely circumstantial or something more lasting? Earlier this year I postulated that fundamental changes were about.

I have been trying to follow the Coal story in China for more than two years, when a series of articles made me realise environmental impacts were creating serious obstacles to continued growth. Coal extraction in China peaked that same year, but is this new trend merely circumstantial or something more lasting? Earlier this year I postulated that fundamental changes were about.

Since then, news have multiplied on the rapid decline of Coal consumption and extraction in China. At first there were reports of an ongoing renewal of the blast furnace fleet, but more recently, it is becoming increasingly apparent that steel consumption has saturated - the law of diminishing returns is catching up with infrastructure deployment. Slowly, this declining trend is looking ever more terminal.

The problem with Coal is the lack of detailed or recent extraction figures on the public domain. In recent times my understanding on this has been exclusively drawn from media articles (most of which were highlighted in the weekly press review). The past few days I entertained an e-mail exchange over this matter with Jean Laherrère, the man with the numbers. Jean retains access to commercial energy databases, from which he is able to draw detailed hindsight. As usual, his view on Coal is better summarised in a few graphs reproduced below the fold.

31 October 2015

Press review 31-10-2015 - Uncertainty

Petroleum prices remain in the flat line around 50 $/b shaped since mid August. Pundits issue forecasts to all tastes, some say the price has to drop further, others that it will have to rise, otherwise even core exporters like Saudi Arabia or Russia will go under. The market reflects this uncertainty, with a good degree of indirectioned volatility. Meanwhile, the Euro sank again below 1.1 against the US dollar this week, meaning an effective rising trend in end products cost.

It is in this environment that comes another blow to heavy petroleum resources, with Shell cancelling an important project in Canada's tar sands. The media keeps touting the mantras regarding Canada: "more oil than Saudi", "enough carbon to cook the planet", but reality is somewhat different. The amount of petroleum extracted from the planet's crust is not only a function of demand, supply also counts. It so happens that these resources are at the moment the most expensive to obtain, therefore the most vulnerable in contraction periods.

It is in this environment that comes another blow to heavy petroleum resources, with Shell cancelling an important project in Canada's tar sands. The media keeps touting the mantras regarding Canada: "more oil than Saudi", "enough carbon to cook the planet", but reality is somewhat different. The amount of petroleum extracted from the planet's crust is not only a function of demand, supply also counts. It so happens that these resources are at the moment the most expensive to obtain, therefore the most vulnerable in contraction periods.

29 October 2015

Convergence Preview - 02 - Frustration

I will start this note with a worn cliché. I was not expecting it to be easy, but I was certainly not expecting it to be this hard. Almost one month later and dozens of hours spent, I still do not have a fully functional Linux desktop operating system running on my Chromebook.

I now feel I have reached a turning point and must try a different approach to this project. Here I report the various methods I tried to get Ubuntu (my desktop system of choice) running on the Acer CB5-311 Chromebook 13, and how they all failed.

24 October 2015

Press review 24-10-2015 - Redesigning the Middle East

Russia slowly settles in as the new sheriff in the Middle East. It is not entirely conclusive what the Russian air-force has achieved, by the Shiite military seem to have found a breeder, with the systematic bombing of high technology arsenals furnished by the US to the Sunni. In the meantime, Iraq is too approaching itself to Russia, seeking a deeper involvement in its war against Daesh.

Ironically, while Russia seeks to tame the threat it sees in the deepening ties between Daesh and the Chechen rebbels, Europe might end up benefiting with a return of some sort of normality to the region, bringing its petroleum assets again on the regular market. But for the moment Europe harvests the seeds of chaos in another neighbouring country with an uncontrollable refugee flow.

Ironically, while Russia seeks to tame the threat it sees in the deepening ties between Daesh and the Chechen rebbels, Europe might end up benefiting with a return of some sort of normality to the region, bringing its petroleum assets again on the regular market. But for the moment Europe harvests the seeds of chaos in another neighbouring country with an uncontrollable refugee flow.

18 October 2015

Portugal: left front government prospect rocks the establishment

"As if we were overthrowing the remainder of the Berlin wall." That is how António Costa, the leader of PS, described the events of the past two weeks in Portugal. Beyond all the metaphors this sentence may carry, it properly conveys the sense of fundamental shift in the country's politics. From the very election night, events took an unusual course, departing from the traditions instituted since the 1974 revolution.

"As if we were overthrowing the remainder of the Berlin wall." That is how António Costa, the leader of PS, described the events of the past two weeks in Portugal. Beyond all the metaphors this sentence may carry, it properly conveys the sense of fundamental shift in the country's politics. From the very election night, events took an unusual course, departing from the traditions instituted since the 1974 revolution.

This note digests the events of these past two weeks and the political choices the country faces. It then reflects on the particularly delicate situation in which the social-democrats now find themselves, to which there are many parallels at the European scale. I then try to anticipate forthcoming developments.

Update 23-10-2015: President Cavaco Silva addressed the country yesterday evening to communicate his decision to appoint Pedro Passos Coelho as prime minister, leaving the right in power. With an uncharacteristic surly tone, the president made clear he will not accept a left front government, calling such solution "inconsistent". The president now hopes for a rebellion within PS to support his government. If that does not happen, Portugal will remain effectively without a government until next March, when Cavaco Silva leaves office.

17 October 2015

Press review 17-10-2015 - 50 dollars

As I write these lines, the Brent petroleum benchmark graph reads exactly 50 $/b. Prices have been hoovering around this round figure for two weeks, lacking major impacting news. This price was crossed sustainably for the first time a decade ago; back then it looked like petroleum was becoming very expensive.

Today, at this same price, it seems the petroleum industry as a whole is about to fall apart. Even if the media remains busier with other matters, the negative news on the industry succeed, from small to large companies, from private to state owned enterprises, no one is left to spare in this market. Much has changed supply side in the petroleum market, the curve is now steeper, and the "easy oil" tail has shrunk considerably. Smoke and mirrors are set up left and right to hide this reality; abnormities such as "peak demand" are employed to fool the fools.

There is no mystery to unravel, no complication to solve, reality is simple and in plain light for everyone to see.

Today, at this same price, it seems the petroleum industry as a whole is about to fall apart. Even if the media remains busier with other matters, the negative news on the industry succeed, from small to large companies, from private to state owned enterprises, no one is left to spare in this market. Much has changed supply side in the petroleum market, the curve is now steeper, and the "easy oil" tail has shrunk considerably. Smoke and mirrors are set up left and right to hide this reality; abnormities such as "peak demand" are employed to fool the fools.

There is no mystery to unravel, no complication to solve, reality is simple and in plain light for everyone to see.

16 October 2015

Convergence Preview - 01 - Unpacking

I was one of the subscribers to the Ubuntu Edge crowd-funding campaign and advertised it here in this space. I believe Convergence is the future of personal computing, the secular electronic miniaturization trend will eventually lead to a single personal computer unit, instead of the myriad devices that litter our workspaces and pockets today. Convergence entails an unprecedented reduction in resources and energy required to manufacture and use a personal computer.

But that was all a long while ago, two years on and the hardware landscape remains pretty much the same. Both Canonical and Microsoft are public in their efforts towards Convergence, but it is yet to materialise.

A couple of months ago Guido Stepken posted the specifications of a laptop computer powered by an ARM mobile processor, the Nvidia Tegra K1. On a first look, the Acer Chromebook 13 provides the same or better than my much battered x86 laptop: a four cores processor, 4 Gb of RAM, a 1080p resolution screen, USB 3.0 ports. Only the 32 Gb of SDD storage leave something to be desired for.

But the most impressive of all is the price: 285 € (VAT included). After some more reading I decided to acquire the damn thing. The goal is to understand how far such architecture can reach in replacing my current laptop.

10 October 2015

Press review 09-10-2015 - Peak Gold

One of the advantages of working for TheOilDrum was the possibility to edit Jean Laherrère's posts. I had a privileged insight into his work and his thinking on the many matters related to resource scarcity he studies. Professional duties made this editing work increasingly difficult and at some point I stopped keeping up with Jean's profuse writing and graphing. Now that TheOilDrum is frozen, Jean Laherrère's graphs are published by Ron Patterson over at PeakOilBarrel.

Back in 2009 I edited a long post by Jean on Gold extraction, that even had to be divided in two parts. Observing secular declining trends on ore grades and extraction volumes in the countries with the largest known reserves, Jean concluded a peak in world extraction was at hand. Yearly volumes kept creeping up a while longer, but the market became increasingly volatile.

In 2013 gold prices divided well below average extraction costs, as private funds in Europe flooded the market with their stocks. The mining industry endured a while longer, but the expected dive in extraction can no longer be adjourned. A return to the record volumes over two thousand tones in 2013 and 2014 seems increasingly unlikely.

Back in 2009 I edited a long post by Jean on Gold extraction, that even had to be divided in two parts. Observing secular declining trends on ore grades and extraction volumes in the countries with the largest known reserves, Jean concluded a peak in world extraction was at hand. Yearly volumes kept creeping up a while longer, but the market became increasingly volatile.

In 2013 gold prices divided well below average extraction costs, as private funds in Europe flooded the market with their stocks. The mining industry endured a while longer, but the expected dive in extraction can no longer be adjourned. A return to the record volumes over two thousand tones in 2013 and 2014 seems increasingly unlikely.

03 October 2015

Press review 03-10-2015 - Life on Mars

Last Monday the media burst in excitement with the discovery of salty liquid water on Mars. From there to "life on Mars" was a baby step and an proper information evening was lost. Mars lacks a far more important essential element to life as we know it: a magnetosphere. The red planet is a dead place, with a cold core and no geological activity. Later in the week came the muffled retractions: it was not really water, just traces of minerals.

It is hard not to compare the life on Mars meme with the "shale oil" revolution. The media behaves just like a herd of sheep, without any sense of direction or critical appraisal; gullibility is their way of being. But soon enough, "shale oil" will acquire a whole new meaning. In Europe the "fracking" speak went totally mute, while in the US the dampened act of contritions emerge, in the wake of a serious financial disaster.

It is hard not to compare the life on Mars meme with the "shale oil" revolution. The media behaves just like a herd of sheep, without any sense of direction or critical appraisal; gullibility is their way of being. But soon enough, "shale oil" will acquire a whole new meaning. In Europe the "fracking" speak went totally mute, while in the US the dampened act of contritions emerge, in the wake of a serious financial disaster.

26 September 2015

Press review 26-09-2016 - The Petrobras jeopardy

The VW scandal with NOx emissions has taken over front pages this week. The climate community seems quite excited with it, as one of the world symbols of fossil fuel combustion falls in disgrace for a most damning cause - lying. It is hard to see at this moment the financial impact the company is to withstand, but it should be something unprecedented.

VW is likely to survive and combustion engines to last. But there are other signs - and far more worrying - pointing to a further declines in fossil fuel extraction in the short term. The present under priced petroleum market is putting a lot of pressure on Petrobras . If up to now it were mostly small companies ailing with 50 $/b, now it is the largest company of the southern hemisphere. Debt rating hawks are out on the prowl and investors scare away.

Petrobras is likely the largest debtor company in the world, with outstanding debt in the order of 200 G$. If it goes down, it will not go down alone.

VW is likely to survive and combustion engines to last. But there are other signs - and far more worrying - pointing to a further declines in fossil fuel extraction in the short term. The present under priced petroleum market is putting a lot of pressure on Petrobras . If up to now it were mostly small companies ailing with 50 $/b, now it is the largest company of the southern hemisphere. Debt rating hawks are out on the prowl and investors scare away.

Petrobras is likely the largest debtor company in the world, with outstanding debt in the order of 200 G$. If it goes down, it will not go down alone.

24 September 2015

Portugal Parliamentary Elections 2015

Portugal is going for regular Parliamentary elections on the 4th of October. The international press wonders now and then why after five years of austerity the political landscape remains apparently unchanged, with the three parties that signed the agreement with the Troika in 2011 still harnessing more than two thirds of the votes in polls.

Portugal is going for regular Parliamentary elections on the 4th of October. The international press wonders now and then why after five years of austerity the political landscape remains apparently unchanged, with the three parties that signed the agreement with the Troika in 2011 still harnessing more than two thirds of the votes in polls.

While it is true that political upheaval seen in Spain, Italy or Greece is yet to materialise in Portugal, the outcome of this election is not as straightforward as might appear on the surface.

This post provides an overview on the election method, the parties with possibilities of electing MPs and the prospects for a resulting government.

19 September 2015

Press review 19-09-2015 - The decline sets in

This Sunday, Greece is going for the third decisive election in less than one year. This time however, it is mostly decisive on a political level. A parliamentary status quo seems likely, without a clear government emerging from the election, but the austerity doctrine seems no longer in question. Portugal is having similar elections in two weeks, and even though harnessing little attention from the international media, a few surprises could be in the pipeline. Watch this space for details in the coming week.

The energy world is well alight in this reentrée. The decline of world petroleum is accelerating and the news meet grinder is in overdrive. The Supply destruction process settles in, with all petroleum exporting nations struggling. There are now hints of a 1 Mb/d decline in the US alone. And more is certainly to come.

The energy world is well alight in this reentrée. The decline of world petroleum is accelerating and the news meet grinder is in overdrive. The Supply destruction process settles in, with all petroleum exporting nations struggling. There are now hints of a 1 Mb/d decline in the US alone. And more is certainly to come.

12 September 2015

Press review 12-09-2015 - Back in business

A confluence of critical events in my professional life has meant an extended summer break for this review. I will be unemployed in a few days, which on the positive side means I might have more time to write. As always, the list of themes I would like to tackle is rather long.

Not much has changed during these past few weeks in the energy landscape. The economic slowdown in China is still dominating commodities markets with a dive in trade between the economies around the Indian ocean. Petroleum prices sank under the 2009 minimum for a few days in August, and the futures curve flattened considerably. Worldwide extracted volumes have been declining since the beginning of 2015 and look far from any bottom.

Petroleum exporting economies struggle: Venezuela, Angola, Canada, Russia... But the felling remains that the worst is still to come and the industry yet to take in the full impact of this under-priced market.

Not much has changed during these past few weeks in the energy landscape. The economic slowdown in China is still dominating commodities markets with a dive in trade between the economies around the Indian ocean. Petroleum prices sank under the 2009 minimum for a few days in August, and the futures curve flattened considerably. Worldwide extracted volumes have been declining since the beginning of 2015 and look far from any bottom.

Petroleum exporting economies struggle: Venezuela, Angola, Canada, Russia... But the felling remains that the worst is still to come and the industry yet to take in the full impact of this under-priced market.

17 August 2015

The cost of the Tesla Powerwall

The public announcement a couple of months ago by Tesla of a medium sized stationary Lithium-ion battery targeting the household market provoked an inordinate reaction. The web erupted with the Powerwall, from exuberant stockholders to mindless criticism, to Forbes' ridiculous claims, every one had a compulsive need to opine over it. I noted the hype and expressed my scepticism towards a technology that seems far from cutting edge in what stationary applications is concerned.

The public announcement a couple of months ago by Tesla of a medium sized stationary Lithium-ion battery targeting the household market provoked an inordinate reaction. The web erupted with the Powerwall, from exuberant stockholders to mindless criticism, to Forbes' ridiculous claims, every one had a compulsive need to opine over it. I noted the hype and expressed my scepticism towards a technology that seems far from cutting edge in what stationary applications is concerned.

{kind=link}

In spite of all the publicity there was little effort to put numbers up for discussion. What is the cost of the electricity generated by a system backed by a Powerwall?

This post is an exercise attempting to answer this question. It presents calculations towards the levelised cost of electricity for a household self-consumption PV system, with and without the Powerwall.

15 August 2015

Press review 15-08-2015 - The dolldrums

It is the middle of August, it is a holyday in much of Europe, but also weekend and most folk are away on vacation. The media is mostly concerned with the influx of refugees, that now occupy traditional holiday destinations. The Brent index hardly moved, staying flat throughout the week at 49 $/b, just an hair off the January lows.

China budged its currency in response to internal economic difficulties ever harder to hide. In the same day the media reported actions by the Chinese Central Bank to depreciate and appreciate the Renminbi. The worrying thing is that apparently this was actually the case.

This review is just a short roundup on the some of the issues followed in this space the last year. Starting by Ukraine, where the Kiev government slowly derides and finds it increasingly difficult to keep its territory together.

China budged its currency in response to internal economic difficulties ever harder to hide. In the same day the media reported actions by the Chinese Central Bank to depreciate and appreciate the Renminbi. The worrying thing is that apparently this was actually the case.

This review is just a short roundup on the some of the issues followed in this space the last year. Starting by Ukraine, where the Kiev government slowly derides and finds it increasingly difficult to keep its territory together.

08 August 2015

Press review 08-08-2015 - Contango deceivance

The Brent index closed a sixth consecutive week of losses under 50 $/b and just an hair off the bottom set last January. The main difference this time is a considerably flatter futures curve; now only in 2017 the future contract fetches a price above 60 $/b. The mainstream media tries to sell the mindless idea that a flatter curve means lower prices for a longer period. In practice this means traders have less of an incentive to store petroleum to sell at a later date, i.e., the supply glut if far less severe this time. But well, these days only the unwary trust the mainstream media at face value.

Various analysts had been for months advertising against what it seemed a growing disconnect between petroleum extraction rates reported by the US government's EIA and the real market. The EIA kept reporting increasing extracted volumes against a backdrop of collapsing prices, declining drilling rigs and asset fire-sales. Cornucopian pundits used this disconnect to foolishly claim the "shale" industry had become efficient enough to be profitable at low prices. But there is no magic here, just a cover up of sorts. And once again we see how the US government is anyything but innocent in this story.

Various analysts had been for months advertising against what it seemed a growing disconnect between petroleum extraction rates reported by the US government's EIA and the real market. The EIA kept reporting increasing extracted volumes against a backdrop of collapsing prices, declining drilling rigs and asset fire-sales. Cornucopian pundits used this disconnect to foolishly claim the "shale" industry had become efficient enough to be profitable at low prices. But there is no magic here, just a cover up of sorts. And once again we see how the US government is anyything but innocent in this story.

01 August 2015

Press review 01-08-2015 - Something must break

There is no bottom in sight for commodities at this moment, and petroleum is no exception. The Brent index closed down for the fifth consecutive week and is now just 3 $/b over the secular bottom set last January. Sour news for the fossil fuel industry in general mar the business pages of the mainstream media: investment deferrals, staff cuts in the tens of thousands, quarterly losses, unavoidable mergers; the spectre of a bankruptcy wave haunts on.

With far less impact on the mainstream media these long months of volatility and under-price petroleum is brewing all sorts of instability among petroleum exporting countries. From Venezuela come news of mass plundering, pointing to an relevant loss of control on the economy by the government. Ailing public finances in Angola foster contest to the regime, that in its turn replies with ad hoc arrests. The UAE is raising petrol prices by 25% overnight.

Something must break. This market is simply not sustainable, part of the supply curve is about to be shaken off. Rest to know exactly which. Will a wave of bankruptcies wipe off the mal-investment in North America? Or will it come down to the implosion of one or more exporting economies?

With far less impact on the mainstream media these long months of volatility and under-price petroleum is brewing all sorts of instability among petroleum exporting countries. From Venezuela come news of mass plundering, pointing to an relevant loss of control on the economy by the government. Ailing public finances in Angola foster contest to the regime, that in its turn replies with ad hoc arrests. The UAE is raising petrol prices by 25% overnight.

Something must break. This market is simply not sustainable, part of the supply curve is about to be shaken off. Rest to know exactly which. Will a wave of bankruptcies wipe off the mal-investment in North America? Or will it come down to the implosion of one or more exporting economies?

25 July 2015

Press review 25-07-2015 - Undue optimism?

Commodities took another deep tumble across the board this week. Staple metals like copper ended the week at decade lows, with fossil fuels dragged down along. China is back to 7% growth, signs of economic recovery are re-appearing in Europe, as for the moment no one dares to question the neo-liberal economic recipe.

The financial world is buoyed by optimism as commodities appear to no longer be the drag on OECD economies as they were the decade heretofore. Reading the news and following financial indexes one gets the sense of an imminent return to the exuberance of the decades that followed the Plaza Accord.

But is at all that good? Has the planet suddenly grow bigger and multiplied its resources? Have all the planetary geo-political issues gone away with the accord on Iran?

The financial world is buoyed by optimism as commodities appear to no longer be the drag on OECD economies as they were the decade heretofore. Reading the news and following financial indexes one gets the sense of an imminent return to the exuberance of the decades that followed the Plaza Accord.

But is at all that good? Has the planet suddenly grow bigger and multiplied its resources? Have all the planetary geo-political issues gone away with the accord on Iran?

22 July 2015

Impressions from FOSS4G-Europe 2015

The conference can only be called a success, fully booked with 400 attendants. This even created some logistic challenges with long food/coffee queues and packed conference rooms. And of course it was great to meet or re-meet the faces behind many useful tools and learn about new software coming down the pipeline.

Here I leave an account of some emerging trends in this field, that may show were FOSS4G is headed.

18 July 2015

Press review 18-07-2015 - An historical Accord

|

Photo by Vahid Salemi. |

Wednesday the second quarter GDP figures for China came out, and are surprisingly high. A wave of optimism swayed the financial world. Another leg down in the Brent index certainly contributed to that.

Only Europe drags its feet, ever more swirled in problems of its own creation. For most Europeans none of this changes much to what remains a bleak outlook.

11 July 2015

Press review 11-07-2015 - China in decline

This was a week of great volatility and uncertainty with Greece and China sending shock waves throughout the world. Commodities in general were beaten up heavily, with Brent trading at prices not seen in many months.

Greece started the week apparently on the verge of precipice, but events rapidly swerved late Thursday. Politically much has changed, but financially things remain pretty much where they were two weeks ago. There is still no comprehensive solution for Greece and the country remains condemned to economic recession.

If Greece fills up front pages in Europe, developments in China can be more important in the long run. The Chinese economy is clearly cooling down with two digit growth figures now definitely behind. In the process the co-habitation of the two economic systems is coming under strain. The media is largely focused on the stock market, but more relevant information is about, with more details pointing to a terminal peak in petroleum extraction.

Greece started the week apparently on the verge of precipice, but events rapidly swerved late Thursday. Politically much has changed, but financially things remain pretty much where they were two weeks ago. There is still no comprehensive solution for Greece and the country remains condemned to economic recession.

If Greece fills up front pages in Europe, developments in China can be more important in the long run. The Chinese economy is clearly cooling down with two digit growth figures now definitely behind. In the process the co-habitation of the two economic systems is coming under strain. The media is largely focused on the stock market, but more relevant information is about, with more details pointing to a terminal peak in petroleum extraction.

04 July 2015

Press review 04-07-2015 - Nai i Ochi

Within hours of the last press review events in Greece developed precipitously with the call for a referendum on the Eurogroup proposals. This Sunday Greeks will be apparently opting between hard labour for life and the cicuta cup. But there is certainly more here than meets the eye, with perhaps more surprises along the road.

At this crucial juncture it is important to look past the debate between those that consider Greeks a chronically lazy folk and those that point the finger to the delusional policies enforced by the creditors. Five years have past since I created the graph below and so far little stock has been taken from it. Growth remains the absolute goal of economic science and practice; ultimately, all policies based on this predicate will fail.

At this crucial juncture it is important to look past the debate between those that consider Greeks a chronically lazy folk and those that point the finger to the delusional policies enforced by the creditors. Five years have past since I created the graph below and so far little stock has been taken from it. Growth remains the absolute goal of economic science and practice; ultimately, all policies based on this predicate will fail.

28 June 2015

Ready for tomorrow?

After all, things in Greece precipitated to an ending within hours of the last press review. Greece was left between the sword and the wall and the Greeks opted for the former. Portugal is next in the line of fire, but an eerie serenity reigns in the country. The mercury is up and most folk are at the beach this weekend; the media speak of football and hockey.

In reality much has changed since yesterday, and Portugal, even if not yet aware, is today a much more fragile country. Events will go sour, and possibly much faster than most expect. Hereby a short list of the gravest developments that are to take place from tomorrow onwards.

In reality much has changed since yesterday, and Portugal, even if not yet aware, is today a much more fragile country. Events will go sour, and possibly much faster than most expect. Hereby a short list of the gravest developments that are to take place from tomorrow onwards.

27 June 2015

Press review 27-06-2015 - Stepping back for the bigger picture

|

This time this reflection can be made through the pen of Herman Daly, with whom the publication of an essay is an event in itself. Daly elaborates on the steady-state economy that will impose itself throughout this century and asks once more for a revision to the goals of Economics. Not only Neo-Classical economics, but also its Keynesian nemesis, were developed with the underlying assumption of infinite growth.

Economic growth is not a physical measurement and as such can grow indefinitely. But in a scenario where the flows of matter and energy through the economic system cease to expand the economic policies used heretofore cease to function as expected. What Herman Daly lays down is a real challenge in this transition, in a dimension that is rarely contemplated.

20 June 2015

Press review 20-06-2015 - stealing the Sun

|

| A man from the past. Photo by Zimbio. |

Naturally not everyone agrees. Some go even further and try to impose the fossil fuel based infinite growth economic model by decree; along the way concentrating economic power in oligopolies. Such is the case with the present Spanish government, lead by Mariano Rajoy. This week one more cog in the energy Manorism system it is trying to impose on its citizens was announced, with a new round of taxes on renewable energy technology.

Spanish folk are not dumb and will certainly have the opportunity to evaluate Mr Rajoy's actions in the general election next November. Less than 5% of the electricity consumed today in Spain is generated by solar technologies; a future oriented government can easily triple that figure with a relevant reduction in cost to consumers.

13 June 2015

Press review 13-06-2015 - Geo-political risks

Geo-political events have clearly dominated the shape of the petroleum curve in the XX century - the post II World War growth, the 1970s OPEC embargo, the fall of the USSR. This century will be no different and Peak Oil will likely be marked by a similar event.

For this reason, this review has followed closely the Sunni-Shiite wars since news broke up of armed combat in Iraqi territory two years ago. The Sunni slowly took control of the Euphrates; the first attacks on Ramadi and Falluja would take place in January of 2014 and six months later the offensive veered northwards. From then these wars spread on to Libya and Yemen.

Behind the scenes two different forms of Islam fence: Arab Sunnism against Persian Shiism. An open conflict would be a world catastrophe, but even if it is avoided, one of these proxy wars can easily unravel and hit the regional source of power: petroleum.

For this reason, this review has followed closely the Sunni-Shiite wars since news broke up of armed combat in Iraqi territory two years ago. The Sunni slowly took control of the Euphrates; the first attacks on Ramadi and Falluja would take place in January of 2014 and six months later the offensive veered northwards. From then these wars spread on to Libya and Yemen.

Behind the scenes two different forms of Islam fence: Arab Sunnism against Persian Shiism. An open conflict would be a world catastrophe, but even if it is avoided, one of these proxy wars can easily unravel and hit the regional source of power: petroleum.

06 June 2015

Press review 06-05-2015 - Peak Coal getting louder

This was a week of nerves as media, markets and pundits tried to guess the outcome of the OPEC meeting yesterday. The cartel did not change their present policy and Brent broke down from its 65 $/b plateau after moments of great volatility.

Meanwhile the Peak Coal talk intensifies. For a decade we got used to see double digit growth figures on everything related to China; an 8% decline in coal consumption in just four months is well beyond unexpected. Almost 2 years ago I wrote a short article on the water demands of the Chinese coal industry; at that time it seemed clear China was reaching the limits of its mining industry and would have to take up a considerable share of the international markets to meet its needs. Facing such scenario, the Chinese government has opted to tackle down consumption and the results are visible. The visions of infinite growth fed on the public by the IPCC and the IEA are now definitely in question.

But is this really the end of the line for coal? It could well be, but I won't be joining the Peak Coal camp so soon. It is not clear yet how fast electricity consumption in China will grow; the price collapse in international markets might drive other countries to extend their consumption a while longer. However, something substantial is clearly changing in the world energy system.

Meanwhile the Peak Coal talk intensifies. For a decade we got used to see double digit growth figures on everything related to China; an 8% decline in coal consumption in just four months is well beyond unexpected. Almost 2 years ago I wrote a short article on the water demands of the Chinese coal industry; at that time it seemed clear China was reaching the limits of its mining industry and would have to take up a considerable share of the international markets to meet its needs. Facing such scenario, the Chinese government has opted to tackle down consumption and the results are visible. The visions of infinite growth fed on the public by the IPCC and the IEA are now definitely in question.

But is this really the end of the line for coal? It could well be, but I won't be joining the Peak Coal camp so soon. It is not clear yet how fast electricity consumption in China will grow; the price collapse in international markets might drive other countries to extend their consumption a while longer. However, something substantial is clearly changing in the world energy system.

30 May 2015

Press review 30-05-2015 - Entering the dolldrums

Commodities markets were generally down this week and petroleum was no exception. The Brent index was particularly hit in the first days of the week but would eventually recover throughout Friday, pretty much to where it started the week. The month of May goes by leaving the index hardly unchanged at 65 $/b.

In terms of relevant news this was in general a quiet week, perhaps reflecting the stagnation in prices. There is some buzz rising above the background noise around a decline of crude inventories in the US. Some claim it is refining picking up ahead of the "driving season", others say the it is "shale oil" extraction giving in to low prices. In reality these are relatively small movements that square well with a nearly flat futures curve. The hard data that will eventually tell who is wrong and who is right in this debate will only be available by year's end.

In terms of relevant news this was in general a quiet week, perhaps reflecting the stagnation in prices. There is some buzz rising above the background noise around a decline of crude inventories in the US. Some claim it is refining picking up ahead of the "driving season", others say the it is "shale oil" extraction giving in to low prices. In reality these are relatively small movements that square well with a nearly flat futures curve. The hard data that will eventually tell who is wrong and who is right in this debate will only be available by year's end.

23 May 2015

Press review 23-05-2015 - Islamic Steamroller

The Islamic State has managed to resume its advances, taking some months to adapt to NATO's involvement in Iraq. In Syria it advances through the south, while in the North al-Qaeda affiliates complete the encirclement to Bashar al-Assad's regime. In Iraq Ramadi was finally taken, after an on-and-off combat that lasted over an year. The Iraqi Shiites are clearly disturbed by another rotund defeat of their US-trained Army. Next in-line to come in the fray are the militias, possibly with weaker training and equipment; right behind them is Iran.

The Islamic State has managed to resume its advances, taking some months to adapt to NATO's involvement in Iraq. In Syria it advances through the south, while in the North al-Qaeda affiliates complete the encirclement to Bashar al-Assad's regime. In Iraq Ramadi was finally taken, after an on-and-off combat that lasted over an year. The Iraqi Shiites are clearly disturbed by another rotund defeat of their US-trained Army. Next in-line to come in the fray are the militias, possibly with weaker training and equipment; right behind them is Iran.

The Brent index seems to be forming a plateau at the moment, clearly below what an healthy petroleum industry requires. Analysts process the figures, scanning for that elusive "peak oil" - 2014 is starting to look a good candidate. In the end it could all be meaningless in face of the swelling Sunni-Shiite wars rocking the Near and Middle East. With bullets flying so close to the most valuable petroleum assets in the world, nothing can be taken for granted.

16 May 2015

Press review 16-05-2015 - Worrying advances

The Brent index closed another week of gains just an hair shy of 67 $/b. Since the beginning of the year the benchmark that prices more than half the petroleum traded internationally has climbed almost 40%. This price is however far from meaning solace to the much battered petroleum industry; the negative outlooks succeed one after the other and every other day the media reports on some troubled company. Some cry "peak oil", likely precipitously. As in the past, the of fate of petroleum will possibly be determined by geo-political events.

Syria has been persistently in the news with the Sunni advancing fast toward the capital. Some media claim the Sunni have received advanced military technology that is decimating the cavalry divisions of Bashar al-Assad's regime. The fall of Damascus appears now a matter of time. The question then is: where will the Sunni turn to next? Will they pursue the western front towards Lebanon, or will they focus on the eastern front in Iraq? Irrespective of the outcome, the Sunni are already regaining the initiative in Iraq, once again attesting to their superior logistics and warfare practice.

Syria has been persistently in the news with the Sunni advancing fast toward the capital. Some media claim the Sunni have received advanced military technology that is decimating the cavalry divisions of Bashar al-Assad's regime. The fall of Damascus appears now a matter of time. The question then is: where will the Sunni turn to next? Will they pursue the western front towards Lebanon, or will they focus on the eastern front in Iraq? Irrespective of the outcome, the Sunni are already regaining the initiative in Iraq, once again attesting to their superior logistics and warfare practice.

09 May 2015

Press review 09-05-2015 - The Tesla hype

This week was marked by the hype created around the stationary battery put on sale by Tesla. The news were out last week, but since there was nothing outstanding about the figures presented, it was not part of the last review. However, the web soon burst with excitement, even with anti-renewables outlets lending a great deal of attention to it.

There is nothing special about the Tesla technology, lagging the competition in various aspects, but the hype is a case study in itself. Almost at the same time Toshiba firmed one more contract with its own stationary Lithium ion technology, that is supposed to last 6 to 7 times longer that Tesla's. To that the media remained widely silent, while on Tesla they went wild. Forbes started by claiming a manufacturing cost of 0.02 $/kWh, meaning it would be essentially free. It then switched discourse to claim that figure was relative to operational costs - but even in that case it still remains ridiculously low.

Once again the media appears little interested in informing the public, it ignores relevant developments while promoting dubious products. As long as the hype lasts there is money to be made in stock markets; but at some point reality settles in. This same dynamics was in great measure responsible for the shale sub-prime bubble.

06 May 2015

Units of Volume

Some weeks ago I was involved in a long e-mail discussion over units of with American colleagues. Arguments went back and forth, but we could not agree on what Tf3 meant.

Some weeks ago I was involved in a long e-mail discussion over units of with American colleagues. Arguments went back and forth, but we could not agree on what Tf3 meant.

I finally came to the conclusion that Tf3 has a different meaning in the US. The unit prefixes used there, even if graphically similar, are not interpreted the same way as the prefixes of the International System of Units (ISU). These differences are likely unknown to most outside the US (like they were to me) and are possibly the source of many errors.

There is also a linguistic twist to this matter that is important to note.

02 May 2015

Press review 02-05-2015 - Still under the waterline

The Brent index is still holding well to its rally, closing the week near 66 $/b. The WTI index, used to price petroleum extracted in the US, is in contrast under 56 $/b, a difference of almost 20%. The price rally is not really happening across the Atlantic, leaving the American industry without relief for now.

Geo-political developments continue to dominate the economic outlook for the years to come, with competing powers continuously challenging the dominant role NATO acquired after the fall of the USSR. There are many points of tension around the globe, which could not possibly be entirely covered in this review. But by focusing on energy flows, it is clear other actors now have a say in the plot of this show.

Geo-political developments continue to dominate the economic outlook for the years to come, with competing powers continuously challenging the dominant role NATO acquired after the fall of the USSR. There are many points of tension around the globe, which could not possibly be entirely covered in this review. But by focusing on energy flows, it is clear other actors now have a say in the plot of this show.

29 April 2015

Footing the bill in Lybia

Muammar Gaddafi visited Europe for the last time in August of 2010, received in Rome with all the honours of a chief-of-state. At the time he requested five thousand million euros from the European Union to help the fight against illegal immigration. His words were peremptory: "Tomorrow Europe might no longer be European, and even black, as there are millions who want to come in".

Muammar Gaddafi visited Europe for the last time in August of 2010, received in Rome with all the honours of a chief-of-state. At the time he requested five thousand million euros from the European Union to help the fight against illegal immigration. His words were peremptory: "Tomorrow Europe might no longer be European, and even black, as there are millions who want to come in".

One year later Gaddafi would be summarily executed at the hands of an Islamic militia.

25 April 2015

Press review 25-04-2015 - Contrasting trends

This was a busy week with multiple developments of interest in energy markets and international politics. Libya is back to front pages, and again for the wrong reasons. However, both the media and politicians remain reluctant in admitting the role of the 2011 European/NATO bombings on the current refugee crisis. The way Italy is being left on its own to deal with the crisis is also quite revealing of the impasse the European Union is in today.

The Brent index extended the current rally, closing the week above 65 $/b, the highest price in over four months. Nevertheless, this price is yet far from bringing solace to the western petroleum industry, that proceeds its haemorrhage of capital and jobs. One of the reasons is the gentle and mooted return of Iran to the international petroleum market, bringing on stream reserves of high EROEI with which international companies can no longer compete.

The Brent index extended the current rally, closing the week above 65 $/b, the highest price in over four months. Nevertheless, this price is yet far from bringing solace to the western petroleum industry, that proceeds its haemorrhage of capital and jobs. One of the reasons is the gentle and mooted return of Iran to the international petroleum market, bringing on stream reserves of high EROEI with which international companies can no longer compete.

18 April 2015

Press review 18-04-2015 - Inversion?

It is not uncommon in commodities markets for an unanimous view to signal a turning point. With the resource optimist media reviewing their outlooks for infinite growth, something was clearly about to change. It just took a few days from the moment the Forbes group declared the "shale boom" dead to a new run up in petroleum prices. Wednesday alone the Brent index climbed nearly 7%, closing the week well above 60 $/b, the highest price since early December.

It will certainly not be this price yet to invert the contraction of the petroleum industry and halt the wave of job losses. But this week trading shows that in first place the price bottom of early January is likely done and secondly that volatility has not gone away.

Soon the media will start guessing where will the petroleum price settle. It will be a pointless discussion, the drivers behind the volatility that brought the price here have not changed.

It will certainly not be this price yet to invert the contraction of the petroleum industry and halt the wave of job losses. But this week trading shows that in first place the price bottom of early January is likely done and secondly that volatility has not gone away.

Soon the media will start guessing where will the petroleum price settle. It will be a pointless discussion, the drivers behind the volatility that brought the price here have not changed.

11 April 2015

Press review 11-04-2015 - Air quality: a driving force

This was a relatively quiet week in the petroleum market, with neither the agreement over Iran's Nuclear programme, nor the raging wars between Sunni and Shiites causing unexpected movements. There is still some volatility but its magnitude is winding down. For the past four weeks the Brent index seems to have settled in the high 50s $/b.

During the largest part of the week a strong polar high parked over north-west Europe before resuming its journey southwards; in many places these were the first real days of Spring. The high pressure imposed by this huge mass of cold air stalled air circulation at the surface and pollution accumulated. By Friday, particulate mater concentrations where prompting public health warnings throughout, with an especial political spin in France, where for the second time this year, restrictions to automotive circulation had to be imposed.

During the largest part of the week a strong polar high parked over north-west Europe before resuming its journey southwards; in many places these were the first real days of Spring. The high pressure imposed by this huge mass of cold air stalled air circulation at the surface and pollution accumulated. By Friday, particulate mater concentrations where prompting public health warnings throughout, with an especial political spin in France, where for the second time this year, restrictions to automotive circulation had to be imposed.

04 April 2015

Press review 04-04-2015 - Agreement or disagreement?

|

Image by Wikipaedia |

These news not only mean some degree of breathing space to the international market (with a particular impact in Asia). For Iran itself means it can now properly care for its ageing petroleum resources, properly managing their inevitable decline.

But is it all good? Considering the reactions from other regional powers that might not be exactly the case.

28 March 2015

Press review 28-03-2015 - Towards a great war

Image by Huffigton Post |

The support NATO provided to the Sunni against the Shiite governments in Syria and Iraq has unleashed a watershed of events that is slowly igniting the whole region. Old rifts are revived, new are open, Sunni and Shiites seem now unable to cohabit peacefully. Under their feet lie the fields that provide more than one third of the petroleum consumed in the world. With Iran and Saudi Arabia on opposite shores, the Persian Gulf could be the stage for the most damaging of wars.

24 March 2015

Coal: a reality check

|

I was particularly intrigued with the CO2 emissions projections in this report. In the standard scenario atmospheric CO2 concentration was projected to reach 1 000 parts per million (ppm) by the end of the century, a near tripling in 100 years. I set out to construct a CO2 emission scenario based on technical fossil fuel extraction projections, and failed to get even to 500 ppm. However, the most fascinating result of that exercise was the relative imminence of a global CO2 emissions peak. Coal represents the largest underground stock of energy and the uncertainty on its ultimate size is high. Notwithstanding, following on the same growth path, a CO2 emissions peak by 2025 was only in reach to the most optimistic Coal extraction scenario. Such is the power of exponential growth.

News of recent days remind again this reality. "Coal bust" is an expression employed to characterise a market that might not be merely conjunctural.

21 March 2015

Press review 21-03-2015 - Transatlantic rift redux

Petroleum prices have endured days of great volatility this past week, with multi percentage point variations intra-day. At the end of the week the Brent index stood pretty much where it started: 55 $/b. Meanwhile the West Texas index (WTI) - the benchmark used to price petroleum extracted across the Atlantic - sank spectacularly to 43 $/b. This means the petroleum sold in the US is now over 20% cheaper than that sold in Europe. Such wide spread is unheard of, and adds another dimension to the rift opening between both continents.

In fact the present WTI levels are but a symptom of an industry out of control, that irrespective of price continues pumping petroleum to fulfil land leasing and other contractual obligations. "Race to the bottom" is an expression used in the US to describe this phenomenon, companies will keep extracting petroleum until they go bankrupt. Many of these companies have adjourned their 2014 balance declarations to the very end of the month, trying to delay as much as possible the day of reckoning.

But the ship is already sinking. The first sizeable American petroleum company went under this week, leaving behind more than 2 G$ in bonds, at best to be restructured, written down at worst. It is unlikely this to be the last company going bust.

In fact the present WTI levels are but a symptom of an industry out of control, that irrespective of price continues pumping petroleum to fulfil land leasing and other contractual obligations. "Race to the bottom" is an expression used in the US to describe this phenomenon, companies will keep extracting petroleum until they go bankrupt. Many of these companies have adjourned their 2014 balance declarations to the very end of the month, trying to delay as much as possible the day of reckoning.

But the ship is already sinking. The first sizeable American petroleum company went under this week, leaving behind more than 2 G$ in bonds, at best to be restructured, written down at worst. It is unlikely this to be the last company going bust.

14 March 2015

Press review 14-03-2015 - Transatlantic rift

|

To almost six years of political turmoil and indecision has compounded the destabilisation of many of the EU's neighbours: Libya, Tunisia, Egypt, Syria and of course Ukraine. The rift opening between the Euro and the Dollar is thus only natural. And this rift is more than monetary. European politicians have much to blame on themselves, for the careless way they discarded Kadaffi and alienated Libya, for precipitously recognising a non-elected Ukrainian government that at best represent half of the population. But the role the US played on all this is ever more evident. And it is ever clearer their objectives are largely antagonistic to our interests.

07 March 2015

Press review 07-03-2015 - Model update season

|

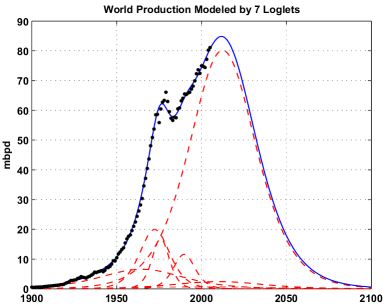

This was perhaps a good moment for an update on the "grand scheme of things", with the publication a week ago of the Loglet Analysis re-run. In a remarkable coincidence, D. Coyle had published an update to the Shock Model, less than 24 hours before. Whilst fundamentally different, the two methods yield similar results: an overall peak within this decade and the loss of some 40 Mb/d between now and 2050. The Loglet Analysis yields a slightly steeper decline, possibly for it is not able at this stage to account for heavy petroleum as well as the Shock model does.

We are standing at the edge, at the edge of our time.

27 February 2015

Loglets Revisited

|

| Remember this graph? |

In reality, volumes extracted grew considerably slower than anticipated by this loglets model. Even if it captured accurately the dynamics of the petroleum system, the decline it portrayed has been considerably delayed. After all this time, how have the results from the Loglet Analysis evolved? Does it portrait a different scenario with eight data points more? This is what this work sets out to answer.

21 February 2015

Press review 21-02-2015 - The real divestment

An out-of-touch campaign calling for divestment from fossil fuels made some fuss last weekend. It gained a good deal of momentum, with calls on major banks to stop financing the fossil fuel industry. Such is the world of cornucopians.

The real world is somewhat different, however. Throughout 2014 this review thoroughly reported how the industry has been cutting back spending, particularly on exploratory activity. This trend formed when petroleum prices still stood above 100 $/b and is driven by a simple fact: the declining quality of remaining resources. This week we learnt the consequences of this divestment: 2014 was one of the worst fossil fuel discovery years since the II World War.

The galore perspective on resources continues to dominate the popular discourse and is one of the main reasons why energy policy has been such a failure in Europe this century. Without acknowledging the profound transformation the fossil energy sector underwent this past 15 years, we remain condemn to failure.

The real world is somewhat different, however. Throughout 2014 this review thoroughly reported how the industry has been cutting back spending, particularly on exploratory activity. This trend formed when petroleum prices still stood above 100 $/b and is driven by a simple fact: the declining quality of remaining resources. This week we learnt the consequences of this divestment: 2014 was one of the worst fossil fuel discovery years since the II World War.

The galore perspective on resources continues to dominate the popular discourse and is one of the main reasons why energy policy has been such a failure in Europe this century. Without acknowledging the profound transformation the fossil energy sector underwent this past 15 years, we remain condemn to failure.

10 February 2015

Press review 14-02-2015 - Back to the past

|

Europe faces enormous challenges in the years, and possibly decades, ahead due to its reliance on foreign imports of fossil energy. By different factors, outright scarcity, geographic constraints or demand growth from competing importers, Oil, Gas and Coal are all set to become harder to afford for Europe. If no other way is provided for the reduction of their usage, then economic hardship shall take care of such task."If you do not deal with reality, reality will deal back with you". These sage words explain what Greece and the EU face: there is no point in slashing GDP if the fundamental issue of the trade balance is not tackled.

07 February 2015

Press review 07-02-2015 - Intertwining

It is interesting how sometimes events intertwine. The ever more complex war in Ukraine is rapidly merging with the stand off over Greece's sovereign debt. The freshly elected Greek government will probably use a veto to further sanctions on Russia as a trump card. Or even threaten to re-approach Russia if a new debt repayment programme is not struck. The geography of all this is nothing short of remarkable.

Europe faces another make or break moment, the frequency of which is less and less reassuring. The more of these D-days repeat the likelier a bad outcome becomes. The Greek democracy can not possibly survive another 4 years of abject austerity, but the masters of the Council seem tightly gripped to their beliefs.

On more mundane matters there was a noticeable rally in petroleum prices, with the Brent index consolidating gains that started late last week. It is however, to little, to late for the industry, and is more likely to signal a bottom than a definitive return to comfortable prices. Midweek I posted an entry level article on what this may mean to the US financial markets.

Europe faces another make or break moment, the frequency of which is less and less reassuring. The more of these D-days repeat the likelier a bad outcome becomes. The Greek democracy can not possibly survive another 4 years of abject austerity, but the masters of the Council seem tightly gripped to their beliefs.

On more mundane matters there was a noticeable rally in petroleum prices, with the Brent index consolidating gains that started late last week. It is however, to little, to late for the industry, and is more likely to signal a bottom than a definitive return to comfortable prices. Midweek I posted an entry level article on what this may mean to the US financial markets.

03 February 2015

Shale sub-prime and the Ides of March

|

| Graphic from Sprott Money. |