In the same period extracted volumes remained too within a narrow band, between 74 Mb/d and 77 Mb/d. Long civil wars in Libya and Syria removed well over 1 Mb/d from the market, with economic sanctions on Iran also having a negative impact. But extraction from source rocks in the US and tar sands in Canada made up for these losses, with a shy output increase in Iraq also helping.

But for how long can this quiet market last? Apart from Iran, the internal politics of every other OPEC member seems deteriorating. Unconventional resources have so far plugged the gap, but can present prices sustain their expansion? In fact there are a few clues pointing to an end to this market sooner rather than later.

1. Backwardation

In first place there are the market data. The future contracts structure in the US has recently formed a pattern called backwardation. This means that cash contracts (for immediate delivery) fetch higher prices than contracts for delivery in months ahead. In this market setting keeping stocks translates into a loss, it becomes more profitable to release stocks onto the market. This contract structure is characteristic of a tight market, with backwardation signalling the immediate need for extra supplies.

Future contracts structure in the Nymex the past few months. Source: Energy Economist.

Future contracts structure in the Nymex the past few months. Source: Energy Economist.

2. IEA calling on OPEC

I have postulated that this remarkable price stability during the past three years has been the fine work of the IEA. The stocks held by the OECD have fluctuated in almost opposite synchronicity to prices: stocks are released when prices rise and built up when prices turn lower.

Two weeks ago the IEA made a public appeal to OPEC members to rise their petroleum extraction. The international agency points particularly to the next winter for an inadequacy of extracted volumes. This may mean this price bounding policy practised so far has run its course.

The IEA refered to existing OECD stocks as "tight by historical standards". This situation is more severe outside the US, expanding internal supply in this country has sustained healthy stocks. Indeed, it seems the IEA has lost its intervention buffer, which by itself may explain the recent shift into backwardation.

3. Constrained exports

On the supply side there are all sorts of constraints. Two OPEC members face civil wars: Libya and Iraq. While extraction rates in the former have already dropped close to nil, in Iraq petroleum output has grown up until recently. The Baghdad government has been slowly loosing ground to the Sunni rebels to the west and the north, now controlling little over one third of the country. This is the third where major petroleum assets lie, but all sorts of energy infrastructure have been targeted by the rebels. A shock to extraction in Iraq is a real possibility, a risk that is leading international companies to retreat from the country. Any policy changes from OPEC must always contemplate a serious disruption to Iraqi output; if the margin exists to absorb it.

Other OPEC members around the Persian Gulf face diverse uncertainties, sparked in great measure by galloping population growth. Several exporting countries face expanding internal consumption by a large young population aspiring to a comfortable life. Difficulties to provide for the needs of this young population may be behind a recent uprising by Shiia populations in Saudi Arabia; and possibly for similar events in Bahrain a couple of years ago.

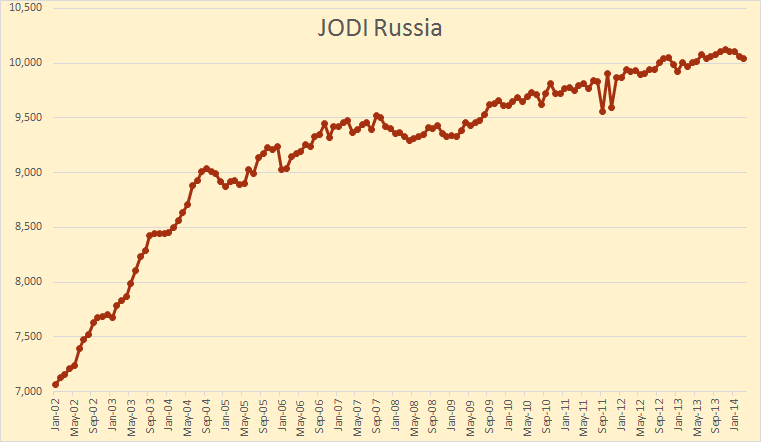

And finally lest not forget the world's largest petroleum extractor: Russia. For years analysts have forecast a short term peak in the country. Output volumes are reported flat for over an year now, and at the moment there seem to be no giant fields left to be brought online to sustain growth.

Petroleum extraction in Russia per the JODI database. Source: PeakOilBarrel.

Petroleum extraction in Russia per the JODI database. Source: PeakOilBarrel.

4. Shale has run its course

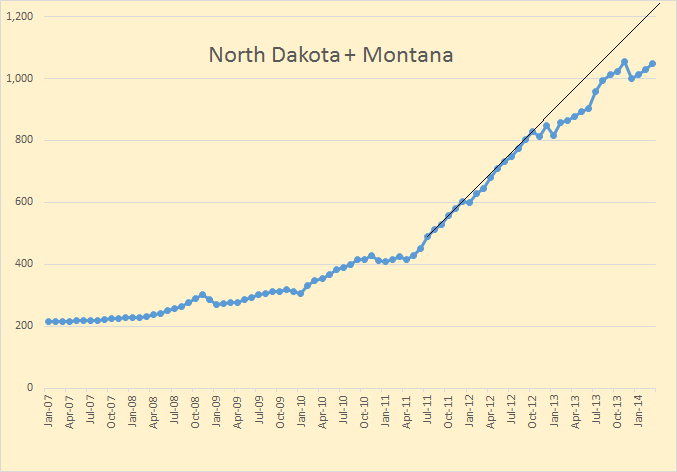

The most important development in the petroleum market these past few years has been the spectacular output growth from source rocks in the US. Petroleum extraction in this country expanded 50% in little less than two years, fostering great optimism and even expectations of energy independence. In recent months this growth has clearly slowed down, with the Bakken formation (Montana and North Dakota) flat since last Autumn. Given the breathtaking decline rates in source rock wells, it is not hard to predict a short term decline in petroleum output from the Bakken. The other major source rock formation, Eagle Ford in Texas, is still well on the growth phase, but may be no more than one year behind Bakken in the extraction curve.

Combined petroleum extraction in Montana and North Dakota per the EIA database. Source: PeakOilBarrel.

Combined petroleum extraction in Montana and North Dakota per the EIA database. Source: PeakOilBarrel.

Still on this point, it is worth noting that a financial crisis of sorts is forming in the US over gas extraction from source rocks. The industry has pledged huge capital resources the past few years without market prices allowing for it to make good on its promises. A sweep of bankruptcies in the sector looms, with yet to be known consequences for petroleum extraction.

5. It never was so expensive to find it

Looking towards the longer term two other trends are important to note: international companies produce ever less petroleum but spend ever more to identify new formations. In recent months most of these familiar companies have been forced (in great measure due to shareholder pressure) into contention policies: selling assets, mothballing riskier projects or even outright cutting spending on exploration. In effect these new policies will translate into a deepening overall extraction decline trend.

International petroleum companies will likely survive these trends, if for nothing else, at least for the knowledge they possess on all sectors of the industry. What these trends flag above all is a concentration of remaining high quality, low risk, high return formations in an ever shrinking set of areas of the world. Novel petroleum frontiers, such as the Arctic or the pre-salt plays in the Atlantic, pose serious risks that cast doubts on their profitability. At least at present prices.

Eventually, something must give. Either demand or supply (or both) must adjust to these developing trends, in a process that is unlikely to be linear, or even swift. Volatility seems set to return.

All of this accords with my view. Let's come back here in 9 months time and compare notes. Thanks for the neat summary.

ReplyDelete'...a process that is unlikely to be linear, or even swift.'

ReplyDeleteViewed on a global scale this volatility may well be represented by a gently falling curve of running averages of production and consumption. But in my view the benign curves of global oil production and price conceal the potential for localised events affecting importers which will be far more severe in their impact on the local economy..

My inquiries of the Oil Majors supplying my own country confirm that they do not have any chapter in their Operations Manuals about how to distribute the oil they can obtain among their customers when the demand (at any price) exceeds the supply available.

So I am led to consider the practical mechanics of how this will happen.

Our refinery picks up the phone and places an order with Head Office of our usual supplier for our ten-daily dose of 130,000 tonnes of crude. We are willing to pay the going price.

Head office replies that they are fffrightfully sorry but yesterday China and India have put in big orders, and the book is empty. Please call again next month, or whenever.

The refinery goes and dips its tanks, and finds it has fifteen day's supply left. The order clerk finishes her lunch, and catches the bus home to Whangerei where she breaks out her EOLAWKI kit and heads for the hills...

We are at the farthest corner of the global oil supply chain, and nobody else will care.

There are many other small importer nations like us who are totally reliant on imports for their economic survival.

Indeed while the ten largest oil importing countries use about 46 million barrels a day (and most of these have some indigenous production), the other 152 oil importing countries (who are mostly fully reliant on imports) use only about 12 million barrels a day. So if a major oil order (or an attack on an oil installation) squeezes global-oil-for-sale on the open market by just one million barrels then it will be about a dozen of those 152 countries who will be most likely to miss out.

They will blink out like lights, and only at year's end will the nations with significant indigenous production notice that our Christmas cards have not arrived.

At the local level it will not be a smooth ride down the back of the curve; it will be very bumpy indeed.