Jorge Nascimento Rodrigues is a free-lance journalist and author, editor of JanelaWeb.com and GurusOnline.tv

Crude Oil

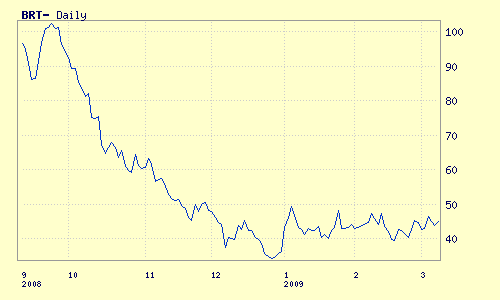

February closing with the barrel close to 45 dollarsCrude oil prices might be back to a mid term bull dynamics, says Australian analyst. February behaved on significant oscillations from one day to the other and the American variety [WTI] climbed 10%, going from 40,78 dollars to 44,76 per barrel.

The minima for the price of a barrel of crude oil, since the peak in July of 2008, might have happened before the Christmas of 2008, advances the analyst from TheOilDrum, Anthony Eriksen, a Canadian mathematician seeded in Sydney, Australia, where he specialized in energy and mining investments.

The conclusion that can be made is that the price of a barrel might be back to a mid term bull trend, after the fall from 145 dollars to less than 50 in the span of only six months last year.

Eriksen reminds that prices of the American crude (WTI) and of the European (Brent) touched then the minima of 31,41 dollars per barrel in 22/12/2008 and 34,04 dollars on Christmas Eve, respectively. This year, the lowest prices occurred last week, on the 18th of February, with values of 34,62 for the WTI and 39,10 for Brent.

The International Energy Agency (IEA) points to a variation interval between 40-45 dollars per barrel, which would still be below the wishes of many producing countries that point to a minimum of 50 dollars for many of the projects they have in scope to be viable, both economically as technologically, underlines the analyst.

The price of a barrel of the American WTI variety reached on the 26th of February a figure slightly above 45 dollars and closed at 44,76 dollars. The Brent vareity closed the month with a price (44,72 dollars) practically identical to the opening figure (44,46).

Daily Brent Blend prices since last September. Source: UpstreamOnline.com; image not in original article.

Wild OscillationsNotwithstanding, the fundamental behaviour of prices during this year has been what some analysts ironically dub “wild oscillations”.

The months of January and February have been fertile with that kind of very close extreme variations; at least 11 cases were observed for the WTI variety solely in February: on 10/2 declined 5% and climbed 10% on 13/2; on 17/2 declined 7% and climbed 14% on 19/2; on 23/2 declined 3,6% and climbed 4,2% on 24/2, 6,6% on 25/02 and 8,5% on 26/2, to go down again on the last trading day of the month. This reveals the high volatility of the agents' behaviour in this market.

To where can these extreme oscillations go and in what measure can the barrel price climb again above 50 dollars or fall below 30 dollars, derives, according to Eriksen, from the “fight” between two heavy weights.

On the one hand the impact of the crisis on the demand of this commodity, continuing to reduce it below 85 million barrels daily (mbd) – the last estimate by the IEA points to 84,8 mbd. This daily figure was still inferior to supply in January of 2009, that was around 85,2 mbd, resulting in a difference of 400 thousand barrels daily.

On the other hand there are several political and physical factors that can influence supply, producing scarcity in the market. Something that didn't happen yet, in spite of the cuts programmed by OPEC, that “should already be enforced in 89% relatively to the commulative cuts announced since September that mount to 4,2 mbd, according to Bloomberg”, says Eriksen.

Black SwansThe analyst underlines that, in the political plane, sudden geoplitics changes in productive regions (namely in the Middle East that continues to be potentially flammable with issues like Israel/Palestine and Iran) or a collapse of the dollar due to the dragging financial crisis or to the political behaviour of the main American currency supporters, can make the crude oil price shot up without previous warning. It would be the surging of inesperate “black swans” to the international scene.

Physical constraints can also have a negative influence on supply. Eriksen refers that the group of oil producing countries outside OPEC seem to have already reached, together, a production peak.

In spite of good perspectives in cases like Brasil (that, nonetheless, can reach “a production plateau around 2011”, according to the studies of this analyst) and Canada for a few more years, global supply from this group is diminishing, with high decline rates in extreme cases like the Gulf of Mexico (around 20%). In 2009 production should decline in Russia, Mexico, Norway and the United Kingdom.

Concerning OPEC a continuation of the programmed cuts policy is to be expected, with a renewal already in the 15th of March, when the cartel meets again. A pressure group formed by Algeria, Iran, Iraq and Venezuela is playing to that tune, according to quotes issued during the last week and a half.

ace adds this final comment:

There remains great uncertainty about key OPEC producer Saudi Arabia's true oil reserves as they are kept as a national secret. The last time that Saudi had a production peak was in 2005 at 9.6 mbd. There is a risk that Saudi Arabia's true crude oil reserves could be much smaller than official estimates implying that future production will stay below the 2005 peak.

No comments:

Post a Comment